Fed to keep interest rates “near zero”

One year ago, the pandemic was upon us as COVID-19’s grip on the United States began in earnest. In anticipation of the coming negative economic impact, the Federal Reserve resolved to take action, including protecting mortgage interest rates.

One year ago, The New York times reported:

The central bank, which restarted its giant bond-buying program eight days ago, said it would expand well beyond the “at least” $700 billion in Treasury and $200 billion in mortgage-backed securities it initially committed to buying. Instead, officials will buy bonds “in the amounts needed to support smooth market functioning”

https://www.nytimes.com/2020/03/23/business/economy/coronavirus-fed-bond-buying.html

Fed reduces support for mortgage interest rates

Contrast that with the recent update from the Federal Reserve’s Federal Open Market Committee (FOMC) statement released March 17, quoted below.

…the Federal Reserve will continue to increase its holdings of Treasury securities by at least $80 billion per month and of agency mortgage‑backed securities by at least $40 billion per month until substantial further progress has been made toward the Committee’s maximum employment and price stability goals.

https://www.federalreserve.gov/newsevents/pressreleases/monetary20210317a.htm

Support has a limited lifetime

While the Federal Reserve still plans to provide artificial support for debt markets and mortgage interest rates, the promised amount is dramatically lower than they announced last year. Furthermore, this support will only last so long…

…until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.

https://www.federalreserve.gov/newsevents/pressreleases/monetary20210317a.htm

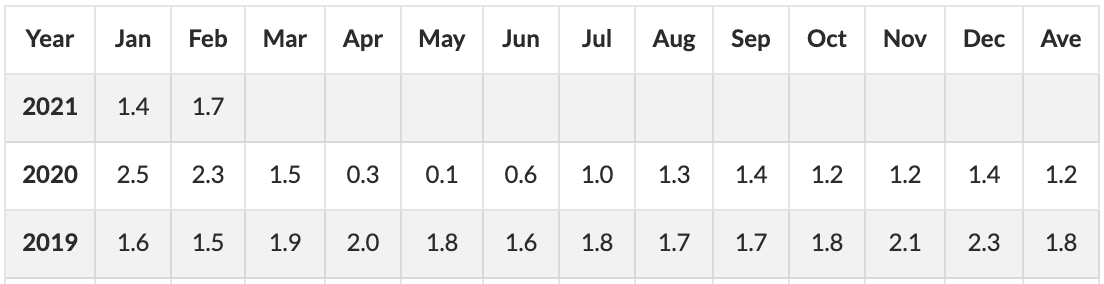

For reference, May 2020 showed the lowest inflation in the last year at 0.1 percent. 2021 shows 1.4% for January, and 1.7% for February. The volatility of the rate of inflation during the pandemic has been cause for concern, and interestingly, the Fed announced the “buy as needed” policy in March 2020 when the inflation rate was 1.5 (down from 2.3 the previous month). The next month (April 2020) saw a near-zero inflation rate of 0.3%. See the chart below for perspective.

As economic projections continue to improve, the Fed’s latest announcement signals cautious optimism, while acknowledging that “we’re not out of the woods just yet.”

If the current housing market has anything to say about it, it’s anyone’s guess. Time will tell.

Housing Inventory is low, and more expensive

Since February of 2020 to February 2021, the national median home price is up 15.8% for existing homes.

Meanwhile, over the same time frame, inventory is down by 29.5%, and is currently at a 2 month supply at current prices.* Below is a live chart of housing inventory as reported by the St. Louis Federal Reserve.

* https://www.housingwire.com/articles/existing-home-sales-dip-6-6-amid-supply-struggles/

A low supply of homes on the market means increased competition for the homes that actually are available, driving up the price.

See also: Tips For Home Buyers In A Low Inventory Market

Home Builders Are Behind

Builders are trying to catch up, but there is a catch: many lumber mills have closed during the pandemic, driving the cost of lumber up.

“The elevated price of lumber is adding approximately $24,000 to the price of a new home,” [NAHB Chairman Chuck] Fowke* said.

https://www.housingwire.com/articles/insane-lumber-prices-mean-new-homes-cost-24k-more/

Scarcity of lumber does more than just drive up costs, however; it delays construction. The amount of inventory added by builders is just not enough to offset the housing inventory deficit.

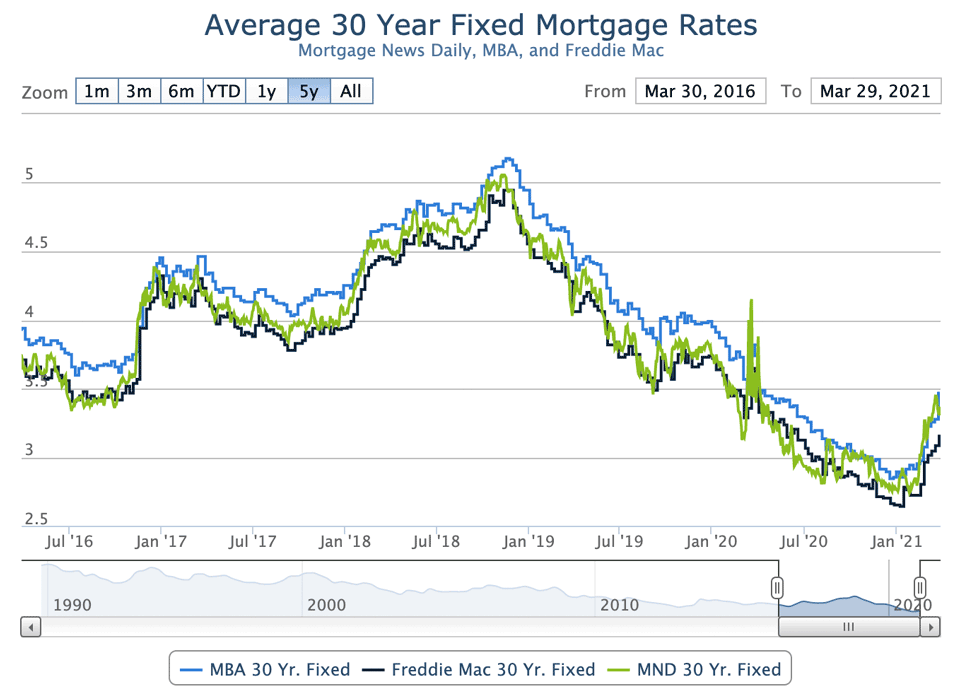

Mortgage Interest Rates begin to rise

The rumors that mortgage interest rates would rise are beginning to prove correct. While these rates are now higher than they were over the summer of 2020 and through winter of the same year, they are still lower than they were at the beginning of last year.

Mixed Signals?

While mortgage interest rates are still slightly lower than this time one year ago, the bad news is that these rates are beginning to rise. If you are a first time home buyer struggling to have your offer(s) accepted, this may end up being good news.

See also: Buy Now To Buy More: What Interest Rates Mean For You

Higher mortgage interest rates means that buying a house is more expensive. I hear you saying, “I thought you said this was good news? How is this good news, exactly?” Supply and demand has a way of balancing out in the long run. In this case, some buyers could be priced out of buying, due to the costs associated with higher interest rates. The resulting decrease in demand could help temper the heat of the housing market down to a more buyer-friendly level.

If the state of the pandemic improves, lumber mills could open, and lumber supplies could improve. Then builders may be better able to help produce more housing inventory.

Is it still a good time to refinance?

The low mortgage interest rates over the past few months have helped spawn a boom in refinance loans, as homeowners saw an opportunity to save.

If you have hesitated to refinance, is it too late?

Yes. No. That all depends. What is your current mortgage interest rate? How long do you plan to keep your home? Is your goal to lower your monthly payment, or to save money in the long run?

For more on the math of refinancing, see The Math of Refinancing: Does It Make Financial Sense?

There are many use cases for a refinance, and the notion that mortgage interest rates are ascending from their storied run through the lowlands isn’t enough to judge every scenario.

For example, if you looking to consolidate debt, a “higher” mortgage interest rate on a cash-out refinance loan is still going to look a whole lot better than credit card debt with a 26% interest rate.

Do you need to take cash out for a renovation, or to pay for college? Both of these are great reasons. This early small rise of current mortgage interest rates isn’t enough to reduce the benefits of a refinance loan.

What can you do in a fast paced, low-inventory housing market?

That’s a good question. In some regions, inventory supply is at less than 1 month. If you are currently in the market for a house, you are in steep competition.

A few articles we’ve published with helpful tips are below.

- Buy Now To Buy More: What Interest Rates Mean For You

- Tips For Home Buyers In A Low Inventory Market

- How to Buy in a Competitive Summer Market

- How to Score in Today’s Housing Market

- Win The Bidding War With Storytelling

With so many homes getting cash offers, you may feel like an offer with a mortgage is a disadvantage.

With Benchmark, we offer a “same as cash” guarantee. What does that mean exactly? It means an offer that has been pre-approved by Benchmark is guaranteed to the seller, by Benchmark.

Learn more about this unique advantage

Contact your local Benchmark branch. Contact us today for personalized information. Call me yourself or request a call from me. WeI would be honored to provide you with our famous excellent service for your new loan.

Benchmark brings you home.